1st Quarter 2026 Outlook

March 3, 2026

Chad Rice, CFA®

Director of Retirement Investment Strategies, Senior Portfolio Manager

Executive Summary

- U.S. corporate pension plans entered 2026 from a position of strength, with funded status levels remaining above full funding for much of the plan universe.

- December market activity modestly improved funded ratios as higher discount rates more than offset mixed asset returns, reinforcing financial resilience across plans of varying maturity profiles.

- Elevated funding levels, combined with attractive pricing in the pension risk transfer (PRT) market, continue to provide plan sponsors with options. Many sponsors are increasingly evaluating incremental de‑risking actions as part of a broader long‑term risk management strategy.

State of the Markets

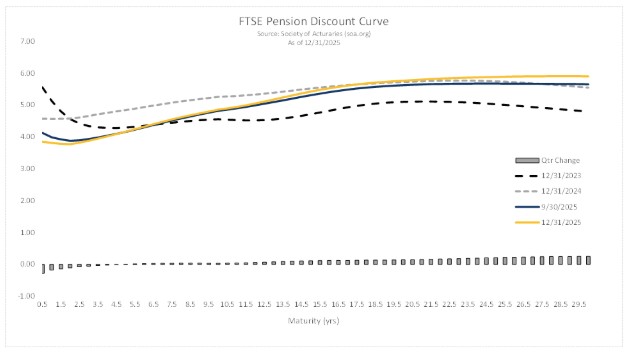

Markets closed 2025 with an increased focus on interest rates and liability valuation. Equity returns were mixed late in the year following strong gains earlier in 2025, while rising treasury bond yields in December, led to lower pension liability values. Across multiple industry monitors, December funded‑status improvements were driven primarily by discount‑rate increases rather than asset appreciation.

Long‑duration yields rose meaningfully during the month, while short‑term rates declined modestly, reflecting expectations for future monetary easing alongside ongoing concerns about fiscal sustainability. These crosscurrents contributed to episodic volatility but ultimately supported pension financials.

Key Economic Influences and Events from Q4 2025

Interest Rates: Higher bond yields late in 2025 reduced pension liabilities by more than 1% for many plans. Longer‑duration plans benefited most from rising discount rates, underscoring the importance of duration management within liability‑driven portfolios.

Inflation and Monetary Policy: Inflation remains above the Federal Reserve’s long‑term target but remains at moderate levels relative to prior years, which is relief to many economists who estimated that the tariffs would have caused a spike at this point in time. The Fed has shifted toward a more balanced posture, with policy decisions increasingly dependent on incoming data rather than a predetermined easing path.

Fiscal and Debt Considerations: Persistent deficit spending and rising interest costs have heightened investor sensitivity to long‑term debt sustainability. As a result, term premiums remain elevated, contributing to volatility at the long end of the yield curve—an important driver of pension liability valuations.

Pension Market Update

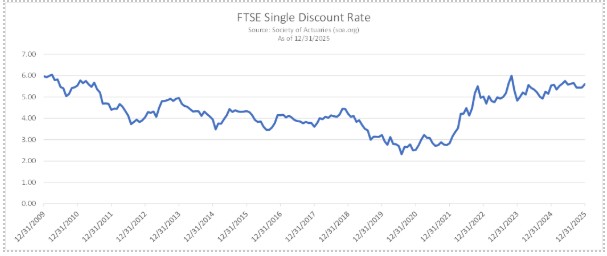

Corporate pension-funded status levels remain historically strong. Aggregate funded ratios increased modestly in December and ended the year on average around 105% based on a sampling of pension funding indices, with December improvements driven primarily by falling liability values rather than asset growth. Over the full calendar year, funded‑status gains were substantial, reflecting favorable capital markets and sustained higher interest rates.

As plans continue to mature and cash outflows rise, sponsors are increasingly focused on aligning asset allocations, liability hedges, and liquidity structures with evolving risk profiles.

Higher treasury bond yields achieved over the year reduced pension liabilities by more than 1% for many plans. Longer‑duration plans benefited most from the rise in discount rates where increased longer rates occurred to the highest extent. Underscore the importance of duration management within liability‑driven portfolios.

Corporate Credit Spreads: Credit spreads remained relatively stable but sit near historically tight levels, offering limited compensation for incremental credit risk. This environment reinforces the importance of quality and issuer selectivity within liability‑hedging portfolios.

Domestic Equity Markets: Equity returns were mixed late in the year following strong gains earlier in 2025. While equities remain an important return engine for many plans, volatility reinforces the value of disciplined strategy and clearly defined risk budgets.

Cashflow and Liquidity: With many plans now paying benefits in excess of 7% of assets annually, liquidity management has become increasingly critical. Sponsors are placing greater emphasis on predictable cash‑flow matching and segmented portfolio structures.

Pension Risk Transfer (PRT) Market: PRT activity accelerated in the second half of 2025, supported by high funded status levels and competitive insurer pricing. Buy‑in transactions reached record quarterly volumes, reflecting increased sponsor interest in locking in attractive pricing earlier in the de‑risking process. While total PRT volume was lower year‑over‑year, activity rebounded sharply from earlier in the year and is expected to remain robust.

Legal Precedent: Legal developments continue to support the long‑term viability of the PRT market. Recent court decisions and regulatory signals reinforce that properly executed annuity transactions remain a permissible and well‑regulated risk management tool for plan sponsors.

Economic Outlook

The economic backdrop entering 2026 remains constructive, though increasingly complex. Growth has continued to surprise the upside, supported by resilient consumer spending, ongoing capital investment—particularly related to artificial intelligence infrastructure—and fiscal stimulus embedded in recently enacted legislation. While inflation remains above the Federal Reserve’s long‑term target, it has moderated relative to prior years, allowing monetary policy to transition away from outright restraint toward a more neutral stance.

At the same time, signs of labor market softening are becoming more apparent. Job growth has slowed; unemployment has drifted higher, and hiring activity has moderated, particularly for entry‑level and white‑collar roles. These trends, combined with persistent inflationary pressures, place the Federal Reserve in a challenging position—balancing the need to support employment without reigniting inflation or undermining long‑term credibility. As a result, policy decisions are likely to remain highly data‑dependent, contributing to continued interest rate volatility.

Fiscal dynamics represent an additional source of uncertainty. Elevated deficit spending and rising interest costs have increased investor sensitivity to long‑term debt sustainability. Markets are increasingly focused on how fiscal policy, trade policy, and monetary policy interact, particularly as tariff decisions and legislative outcomes influence growth expectations, inflation dynamics, and Treasury issuance. These factors have contributed to a higher term premium, reinforcing volatility at the long end of the yield curve.

For corporate pension sponsors, this environment underscores the importance of maintaining flexibility. While higher interest rates have materially improved funded status outcomes in recent years, volatility around rates and spreads remains a key risk. The path forward is unlikely to be linear, and sponsors should expect periodic episodes of risk‑off behavior as markets digest evolving policy signals and macroeconomic data.

Investment Strategy

Given the current macroeconomic environment, a disciplined and risk‑aware investment approach remains appropriate for corporate pension plans. Elevated funded status levels provide sponsors with optionality, but they also increase the importance of protecting gains already achieved. With interest rates remaining higher than their long‑term averages and credit spreads near historically tight levels, the margin for error has narrowed, particularly within return‑seeking and credit‑oriented allocations.

From a liability‑hedging perspective, maintaining alignment between asset duration and liability characteristics remains a core priority. Interest rate volatility has become a more prominent driver of funded status outcomes, reinforcing the value of hedge discipline and well‑defined rebalancing frameworks. While long‑term yields may remain range‑bound over the intermediate term, episodic spikes driven by fiscal or policy concerns can materially impact liability valuations, creating both risks and opportunities for sponsors positioned to act.

Within fixed income portfolios, quality remains paramount. Credit spreads currently offer limited compensation for incremental risk, suggesting a preference for higher‑quality issuers, diversified exposure, and selective sector positioning. This approach aligns with the dual objectives of income generation and capital preservation, particularly as markets remain vulnerable to shifts in growth expectations or emerging credit stresses.

Liquidity management continues to grow in importance as more plans transition deeper into net cash‑outflow status. Structuring portfolios to meet predictable benefit payments while retaining flexibility for rebalancing and opportunistic actions is increasingly critical. This includes thoughtful segmentation of assets, proactive cash‑flow planning, and ongoing evaluation of how return‑seeking assets fit within the plan’s broader risk management framework.

Finally, elevated funded levels and competitive pricing continue to make pension risk transfer an attractive strategic consideration for many sponsors. Whether executed incrementally or as part of a longer‑term end‑game strategy, annuity transactions can serve as a powerful tool to reduce volatility, simplify governance, and lock in funded status gains achieved over recent years. In this environment, proactive planning and readiness remain essential.